Greetings to Our Partners

As we begin the new year, we want to thank you for your continued partnership and trust. The early part of the growing season is focused on planning, field preparation, and closely monitoring weather and water conditions that will shape the 2026 crop.

While it is still early to determine final production levels, initial observations across California and the Pacific Northwest are beginning to provide insight into planted acreage, crop progress, and regional water conditions. Our teams remain actively engaged with growers and industry partners to monitor these developments and share clear, practical updates as the season moves forward.

California Tomatoes

According to early USDA processor reporting, California’s contracted processing tomato volume for the 2026 season is currently estimated at approximately 9.8 million tons, reflecting a significant reduction in California processed tomato tonnage. Contracted acreage is expected to total roughly 185,000 acres statewide.

Growers are currently estimating yields near 53 tons per acre based on contracted acreage projections, but with a 10-year average closer to 50 tons per acre, it is possible the overall crop could come in under current projections

California Water & Snowpack Conditions

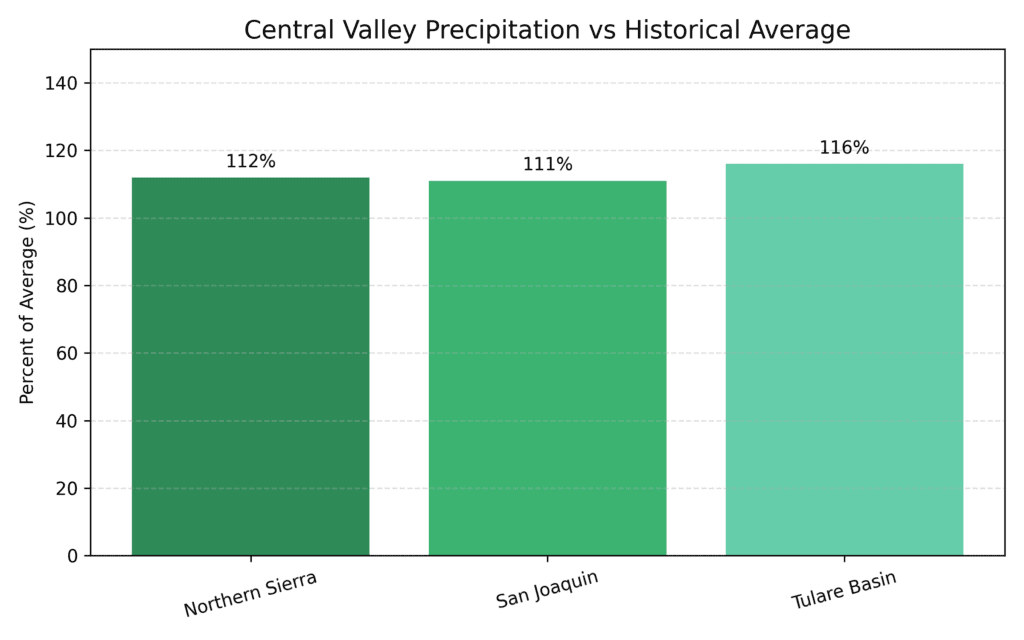

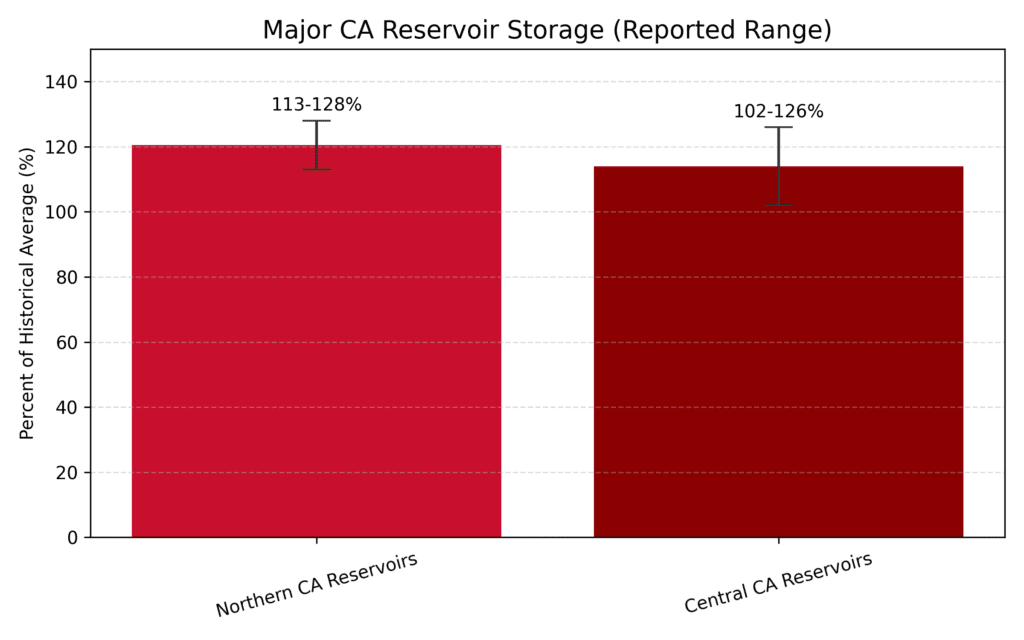

Water and growing conditions across California are generally trending in a favorable direction as we move toward the 2026 processing tomato season. Key Central Valley precipitation indices are running above average to date, and major reservoir storage remains above historical averages for this time of year. Recent water allocation announcements were somewhat more conservative than earlier expectations, particularly on the federal project side. While current reservoir storage and precipitation levels remain supportive, allocation levels will continue to be monitored closely through the spring as final supply outlooks are refined.

At this stage, we believe water availability should support a stable 2026 crop; however, some uncertainty remains typical for this point in the season.

Source: California water and reservoir reporting (March 2026). Values reflect current conditions relative to historical averages and are intended to provide directional insight as the season develops.

Pacific Northwest Fruit

Pears

Early indicators across the Northwest pear industry suggest continued structural adjustment heading into the 2026 season. Field observations and task force input indicate that orchard removals and crop load trends are likely to reduce overall available volume compared to recent years.

Orchard Removals & Acreage Shifts

Recent grower reporting indicates that 300–500 acres of Northwest pear orchards are already expected to be removed, with additional acreage still under review. In some areas, removals have already begun, including reductions in key varieties such as Bartlett.

Regional task force discussions suggest that total removals could ultimately reach approximately 1,000 acres, although it remains uncertain how much of that acreage will be removed during the 2026 growing season.

Based on industry average yields of 20–25 tons per acre, removals at that level could represent roughly 20,000– 25,000 tons of potential production capacity over time.

Market Balance & Cannery Demand

Industry and task force discussions point to a tighter supply balance heading into the season. Fresh market volume is expected to remain in the 100,000–105,000 ton range, though orchard removals may further limit available supply.

Cannery demand expectations have adjusted lower, with 30,000–35,000 tons now viewed as a more realistic planning range for the 2026 pack season, compared to prior planning levels closer to 50,000 tons.

Water Supply Conditions

Water availability remains an important factor for tree fruit regions. Current snowpack levels are tracking at approximately 41–49% of long-term averages, which will influence irrigation planning. Recent rainfall has improved reservoir storage, but additional snowpack accumulation will be needed to support spring and summer water demand.

Costs

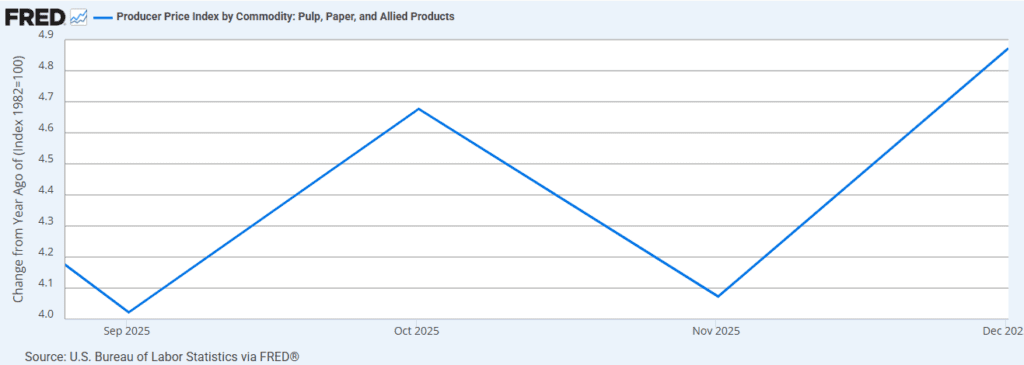

Corrugate

Corrugate stayed relatively steady throughout 2025. Early 2026 there was announcements by some of the conglomerate corrugators of close double digit increases for the general market. While demand has slowed, capacity has been reduced along with some plant shut-downs. Certain contracted customers align with tonnage rates published by Pulp & Paper Weekly (PPW) which will be coming out in mid-March and anticipating lower impacts than announced.

Note: These charts reflect broad market trends (year-over-year change), which may differ from contracted costs and timing.

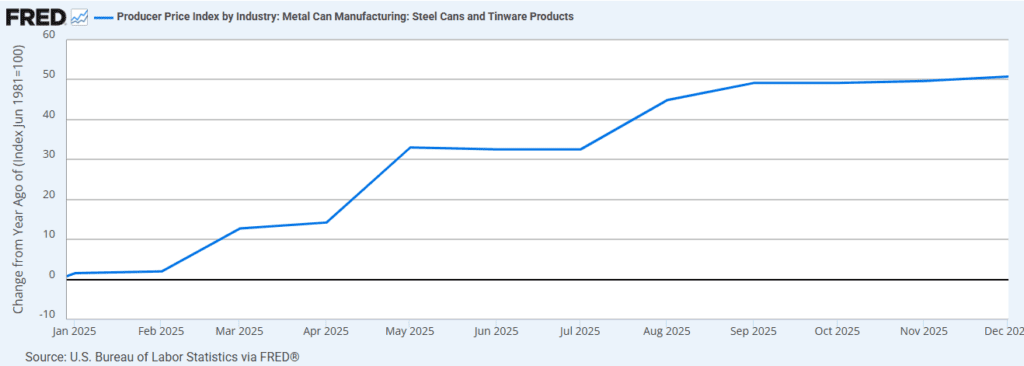

Cans

Steel prices have increased primarily impacting tinplate which due to higher demand outlook for data center constructions and AI technology (tin plate being used in circuit boards). Tin mill producers were also less willing to share the tariff burden going into 2026 putting further cost pressure for food cans.

Tariff rates have varied based on the regions can manufacturers are sourcing metal, and the US currently only has the capacity to support approximately 30% to total food can demand. There is recent news from the Administration in relieving tariffs for certain products that do not present a threat to the US under the IEEPA. Depending on outcome, this could potentially relieve cost pressure but would take some time for can makers to work through tariffed inventory before that could come to fruition.

Corn Syrups

There were a lot of late bookings from buyers who contract directly with toll processors in Q4 of 2025. Originally, costs were anticipated to stay flat due to strong export demand and potential cost increases passed on by millers. However, companies contracting later saw some price relief due to soft demand and favorable crop outputs.

Sugar

Overall demand has been soft, along with excess inventory in the U.S. GLP-1 usage and restrictions to SNAP benefits are large contributing factors. Beet sugar yields saw strong results, which compete with cane sugar, further reducing costs and coming close to bottoming out. There comes a point where U.S. sugar processors will sell off inventory through government subsidies, converting sugar to biofuels. This would cause a price increase, as global suppliers would be able to leverage lower domestic inventory to increase the cost of imported sugar. Our buyers have watched the market in an attempt to secure the best possible pricing.

Oils, Spices & Dehydrated Ingredients

Due to the seasonality of various ingredients, results vary based on the growing region, supply and demand, and tariffs. Domestic salt is seeing increases due to operational costs and the high cost of steel for infrastructure, while pepper outlooks are currently stable. Oregano pricing is volatile. There continue to be supply constraints, poor crop yields, and high demand. Acres planted have reached historic lows, and shortages beginning in 2023 have created further gaps in future supply. Current crop expectations anticipate a shortage of 3,000 to 4,000 MT for 2026. Egyptian oregano is recovering, but not enough to fulfill the large supply gap.

For other ingredients, there have been some indications of flat pricing to possible price relief on certain dehydrated ingredients, but we will know more in March.

Regarding oils, declines in yields and reduced planted acreage have impacted EVOO and sunflower oils, and a weakened U.S. dollar has shown indications of increased cost pressures. Many buyers will sometimes shift demand to alternate oils, which can create volatility in otherwise stable oil markets. Domestic soy is likely the most stable, with ample supply and a decline in export activity.

Thank you for your continued partnership. We wish you a healthy and successful season ahead and look forward to sharing our next Crop Report in the coming months as further clarity develops around weather, water, crop conditions, and broader market factors.

The Neil Jones Food Company